Vice President Dr Mahamudu Bawumia delivered a public lecture on Ghana’s digital economy on Tuesday, November 2, 2021, at Ashesi University. He said the current administration had made some monumental gains at digitising Ghana as never witnessed since independence.

Fact-Check Ghana has verified some of the claims and found them to be false and misleading. Here are the claims and the verdicts:

Claim 1: “Again, I believe the motor insurance database I believe I don’t know of any African Country that has put together this motor insurance database. Ghana is the first to do so.”

Verdict: Completely False

Explanation: Ghana began implementing the Motor Insurance Database on January 1, 2020, to provide a centralised system from which security agencies and the general public, including passengers of vehicles, could check the validity of vehicle insurance instantly.

But before Ghana took this initiative, some African countries had undertaken massive projects that compiled a comprehensive database of the motor insurance sector 10 years before Ghana’s rolled out.

One of such countries is South Africa.

The South African Insurance Association established a database in 2008, to fight insurance crime, especially also insurance fraud.

On its website, the Association said it was instrumental in establishing the South African Insurance Crime Bureau (SAICB) at the end of 2008.

A new Vehicle Salvage Database was launched in May 2018 in South Africa to address the shortfalls of the old system, which authorities say had some deficiencies.

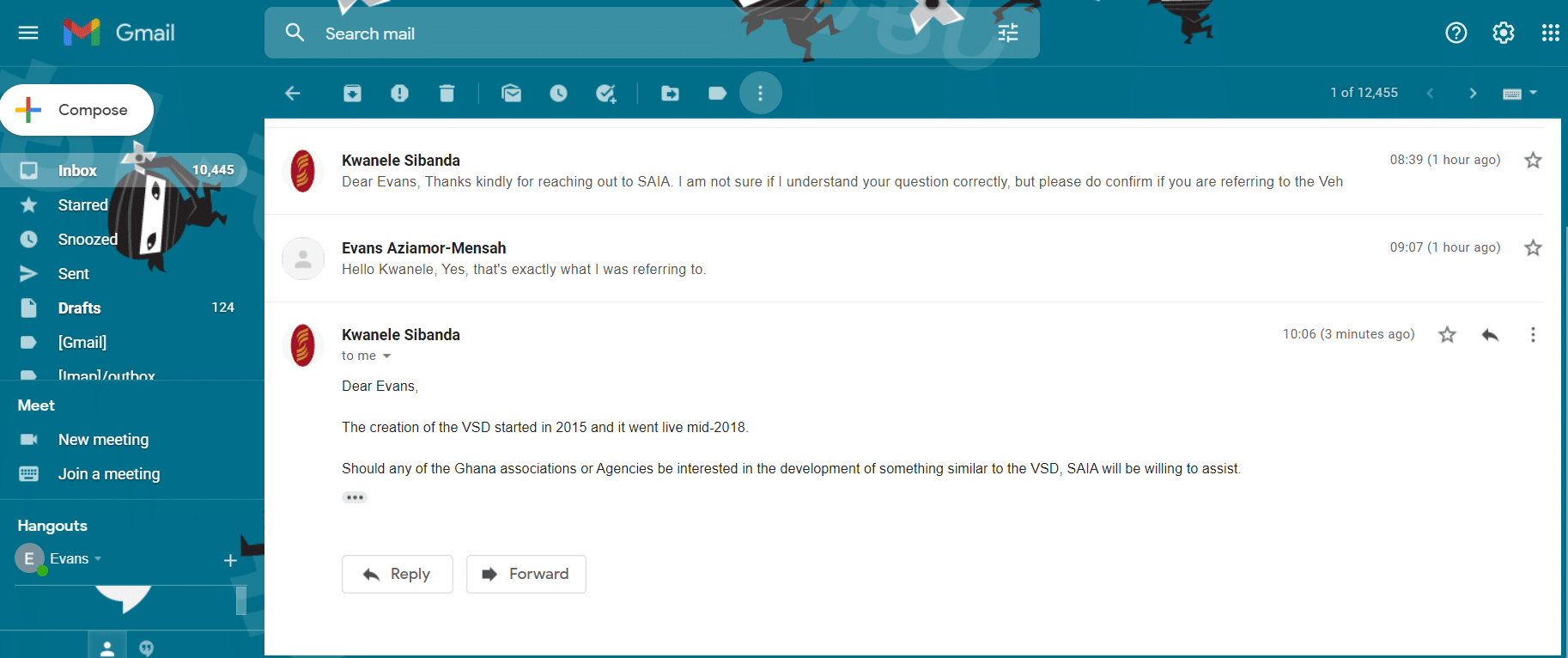

In an email correspondence between Fact-Check Ghana and the Corporate Affairs Office of The South African Insurance Association (SAIA), the Office stated that “the creation of the VSD (Vehicle Salvage Database started in 2015 and went live in 2018”

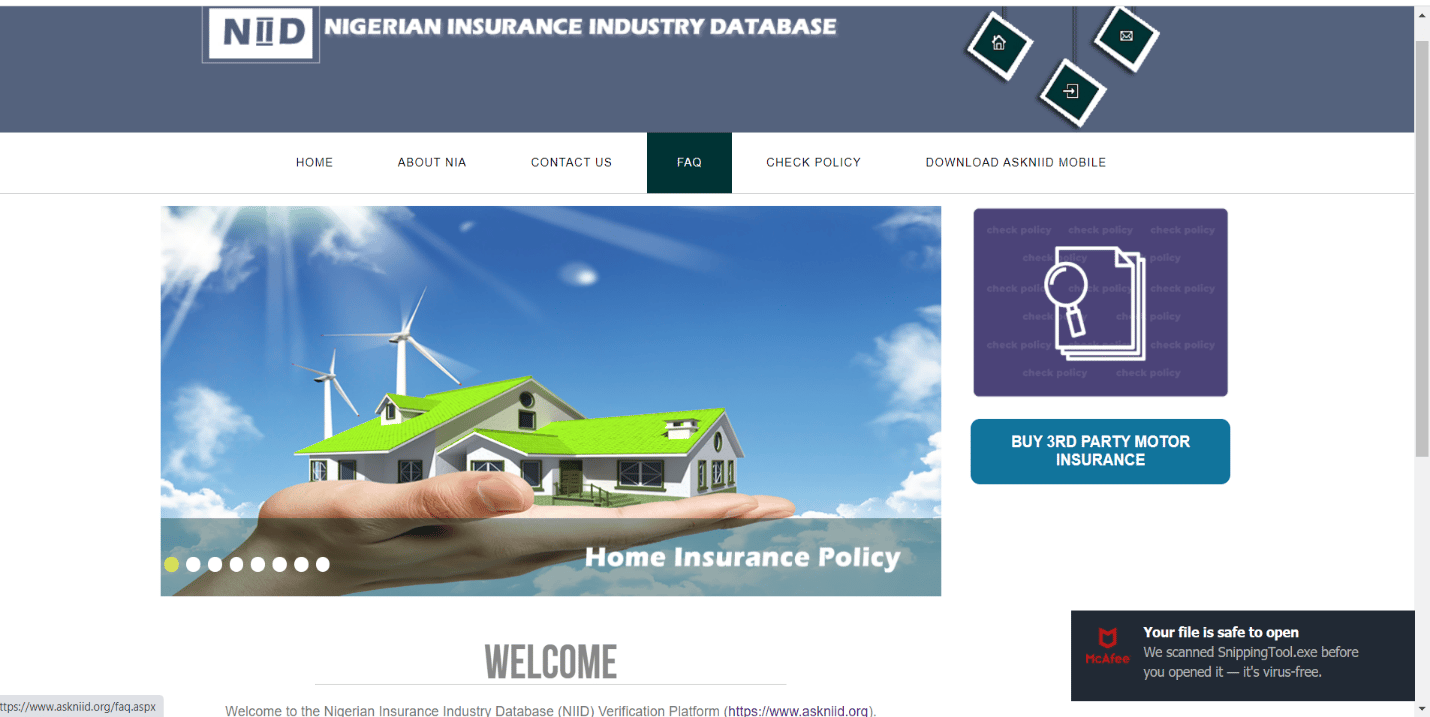

Another country, the biggest economy in West Africa, Nigeria has had this project in place since 2009.

Nigeria’s Insurance Industry Database (NIID) was meant to get rid of fake motor insurance certificates on Nigerian roads, the menace of fake insurance papers and insurance racketeers.

The Director-General of the Nigerian Insurance Association, Yetunde Ilori, in an interview with the media in July 2020 said “the NIID system, now in its 10th year of implementation, has been effective in transforming the motor insurance policy landscape of the industry,” adding that the NIIP – a unified platform for the sale of Motor Third Party Insurance cover, had since been deployed and is running live for business transactions.

In 2019, the Association said it generated about N196 million from data upload on the Nigerian Insurance Industry Database (NIID) in the 2019 business operation.

Claim 2: “…Ghana is the first country in Africa … to achieve this type of interoperability between bank accounts and mobile wallets…”

Verdict: False

Explanation: The Ghana Chamber of Telecommunications, together with the Government of Ghana, the central bank, GhIPSS and commercial banks on 10th May 2018, launched the first phase of the mobile money interoperability system.

The Mobile Money Payment Interoperability is the service that allows direct and seamless transfer of funds from one mobile money wallet to another mobile money wallet across networks. It was developed by Ghana Interbank Payment and Settlement Systems (GhIPSS) with the active collaboration of the telecom industry.

Six months later, on Wednesday, November 28, 2018, the second phase of the project was launched.

Dr Bawumia said the launch completed the “Financial Inclusion Triangle because it interconnects three payment platforms; mobile money, bank account and e-zwich.”

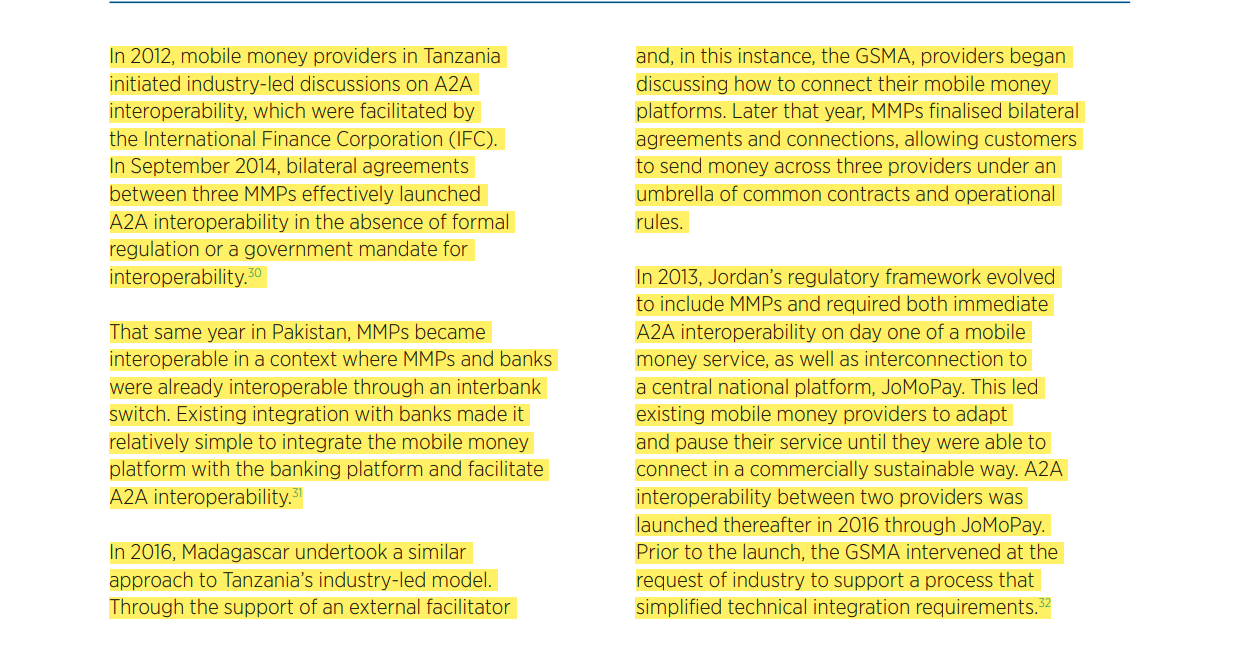

Before Ghana had contemplated this move, Tanzania was already benefiting from the usage of the mobile money interoperability system.

In September 2014, a GSMA report on Tracking the Journey Towards Mobile Money Interoperability noted that Tanzania effectively launched Account to Account interoperability to facilitate payments by mobile networks.

“Indeed, there’s precedent in Tanzania, the first African country to adopt interoperability, where there has been increased transactions among users. It’s a measure that’s also been adopted in Kenya and Ghana,” the report partly reads.

An excerpt of the report

Fact-Check Ghana also spoke with some Tanzanian citizens to confirm if indeed the type of interoperability between bank accounts and mobile wallets works in the country.

“Yes, it’s very convenient to send money from one’s mobile account to a different mobile account or bank,” Hussein Bin, a photographer and youth activist in Tanzania, said. He added that the “charges for the services differ depending on the bank”.

Asked if the type of interoperability works in Tanzania, Lilian Alex, a programme assistant with the East African Civil Society Organisations Forum (EACSOF), based in Arusha, said “Yes, it does.” She confirmed that she has ever used it.

That same report, Tracking the Journey Towards Mobile Money Interoperability, also mentioned Pakistan as the country where Mobile Money Payments and banks were made interoperable through an interbank switch in 2014.

Two other African countries Madagascar and Kenya followed next in 2016 and 2017 respectively.

Far away in Jordan, JoMoPay, an interoperability platform was fully implemented in 2016, all in the bid to promote financial inclusion.

It is, therefore, not true that “Ghana is the first country in Africa … to achieve this type of interoperability between bank accounts and mobile wallets.”

Editor’s note: In the initial report, we indicated that South Africa in 2008 rolled out a National Insurance Database before Ghana. Further checks indicate that the South Africa database was for salvaged vehicles.