Kojo Oppong Nkrumah, Member of Parliament for Ofoase Ayirebi Constituency, has alleged that the Mahama-led government had introduced new taxes on the blind side of Ghanaians.

He made the claim during an interview on Okay FM’s “Ade Akye Abia” morning show, asserting that while the government repealed three taxes, it secretly introduced others. Similar claims have been made by other members of the opposition New Patriotic Party (NPP).

These statements followed Parliament’s approval of several tax amendment bills in March 2025, reportedly aimed at enhancing revenue efficiency and realigning key government funds to drive national development. These changes included the repeal of the Electronic Levy (E-levy), the 10 per cent withholding tax on betting and gaming winnings, and the removal of the 1.5 per cent withholding tax on unprocessed gold from small-scale miners. The bills were subsequently assented to by President John Dramani Mahama at a signing event held on Wednesday, April 2, 2025.

“…He [President Mahama] signed for three or four taxes that both the NDC and NPP members in the previous Parliament had already agreed should be scrapped in 2025. At the same time, he also signed new bills introducing about four new taxes proposed by the NDC government. However, if you listen to their communication, they have hidden the new taxes they introduced,” the former Minister for Works and Housing stated. He also listed some taxes he claimed the government had newly introduced.

Fact-check Ghana has verified the claims and presents the facts below.

Claim 1: “They have also introduced a tax which applies to banks, financial institutions, and trading companies, it is called the Growth and Sustainability Levy, which is five per cent and is starting in 2026, 2027 and 2028.”

Verdict: Misleading

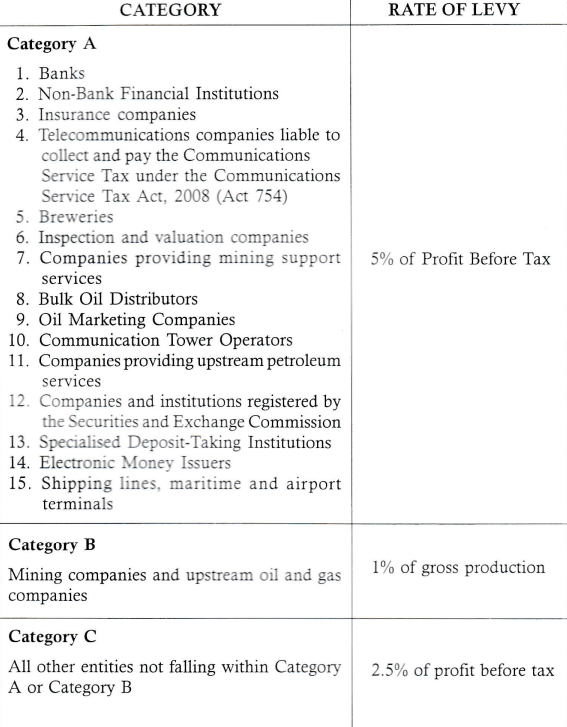

Explanation: The Growth and Sustainability Levy Act, 2023 (Act 1095), was enacted to replace the National Fiscal Stabilisation Levy Act, 2013 (Act 862). Under the new law, a five per cent levy is imposed on specific categories of companies, including banks, financial institutions, and trading companies.

Although the five per cent tax rate remains unchanged, the government has extended the law’s sunset clause from 2025 to 2028, as stated in the national budget. This extension means that the Act, originally set to expire in 2025, will now remain in effect for an additional three years.

Dr. Julius Gyimah, a fiscal policy expert and Executive Director of the Centre for Economic and Financial Analysis (CEFA), explains that while the rate has not changed in form, the extension effectively reintroduces the tax in substance.

Therefore, contrary to claims by Kojo Oppong Nkrumah, the basis of the tax is not new; the reality is that the government has prolonged a levy that was intended to be phased out.

Below is a table showing the tax rates applied to specific categories of companies under the Growth and Sustainability Levy Act.

.

Source: Growth and Sustainability Act, 2023

Claim 2: “The third tax that they have introduced that they don’t talk about is the growth and sustainability levy for mining industries. They have introduced a 2 per cent levy on gross production.”

Verdict: Misleading

Natural resource rent, which is the difference between the revenue earned from a mineral commodity and the average cost of producing it, constitutes about 14 per cent of Ghana’s GDP. Yet, revenue generated from the extractive sector accounts for only around 1.5 per cent of GDP. According to the minister, this is largely due to the country’s inability to fully capture the economic rent from natural resources.

Despite the recent surge in global gold prices, Ghana has not been able to maximise the potential benefits. To address this, the government has proposed increasing the Growth and Sustainability Levy on the gross production of mining companies from 1 per cent to 3 per cent. Additionally, the sunset clause of the levy, originally set to expire in 2025, has been extended to 2028.

Dr. Gyimah, a fiscal policy analyst, asserted that laws like the Growth and Sustainability Levy Act are typically designed with fixed durations, governed by “sunrise” and “sunset” clauses that define their start and end dates. These laws are meant to be temporary, serving specific policy objectives within a set timeframe.

The Act, introduced in 2023, was set to expire in 2025. As such, the expectation was that the Minister for Finance would repeal the levy in the 2025 budget, marking the end of its intended three-year lifespan.

However, the decision to extend the levy beyond its original timeframe, Dr. Gyimah notes, reintroduces the tax, contrary to the law’s initial intent.

“The original law stipulated that the tax would end in 2025,” Dr Gyimah noted. “Now, not only is it continuing, but the rate is being increased from 1% to 3 per cent, and the sunset clause is being extended by another three years.”

He added, “The form is that it is an existing law that was introduced by the previous government, but in substance, looking at the treatment of it, it means that you are bringing in a new tax. So it’s a matter of substance over form, but if we are looking at the legal form over substance, then it is just an existing tax that has been amended.”

Claim 3: “The last one is a new tax that they have introduced at the ports called the Special Import Levy, so from 2026, 2027 to 2028, anyone who clears their goods at the port will pay the newly introduced Special Import Levy.”

Verdict: Misleading

Explanation: The Special Import Levy was introduced under the Special Import Levy Act, 2013 (Act 861), and applied to imported goods at the point of entry. A levy of 1 per cent was imposed on machinery, equipment and fertilisers, while a levy of 2 per cent applied to all other goods, excluding petroleum products. The 1 per cent levy on machinery, equipment and fertilisers was, however, scrapped in 2017 by the Special Import Levy (Amendment) Bill, 2017.

Like the Growth and Sustainability Levy, the initial position of the law was that it was supposed to be repealed in 2015, as that marked its sunset clause. The amendment in 2017 extended the sunset clause to 2019.

In the 2020 budget statement, the Finance Minister, Ken Ofori-Atta, announced that the Special Import Levy was to be extended for another five years. This means that the levy was to expire in 2025.

The new government’s announcement in its budget statement is further extending the sunset clause of the Special Import Levy from 2025 to 2028.

This makes Kojo Oppong Nkrumah’s claim that the government is introducing a new tax in the name of the Special Import Levy misleading.

While recent claims suggest the introduction of entirely new taxes, a closer examination of the legal and fiscal framework reveals that most of these levies, such as the Growth and Sustainability Levy and the Special Import Levy, are not new. Instead, they are existing taxes that have either been clarified, adjusted, or extended beyond their original end dates.

“The only thing that we can boldly say is a new tax without any narrative is the reintroduction of the road toll, which is captured in the budget and expected to be implemented later in 2025. The ones above are just existing, they come and they are changed just like that.” Dr Julius Gyimah said.